The Two Facts You Need to Hold Together

Harvard economics professor Jason Furman's analysis of H1 2025 data produced a number that should have stopped more people in their tracks. The data processing sector (which includes the companies building and operating AI infrastructure) represents roughly 4% of total US GDP. In the first half of 2025, that sector accounted for 92% of all US GDP growth.

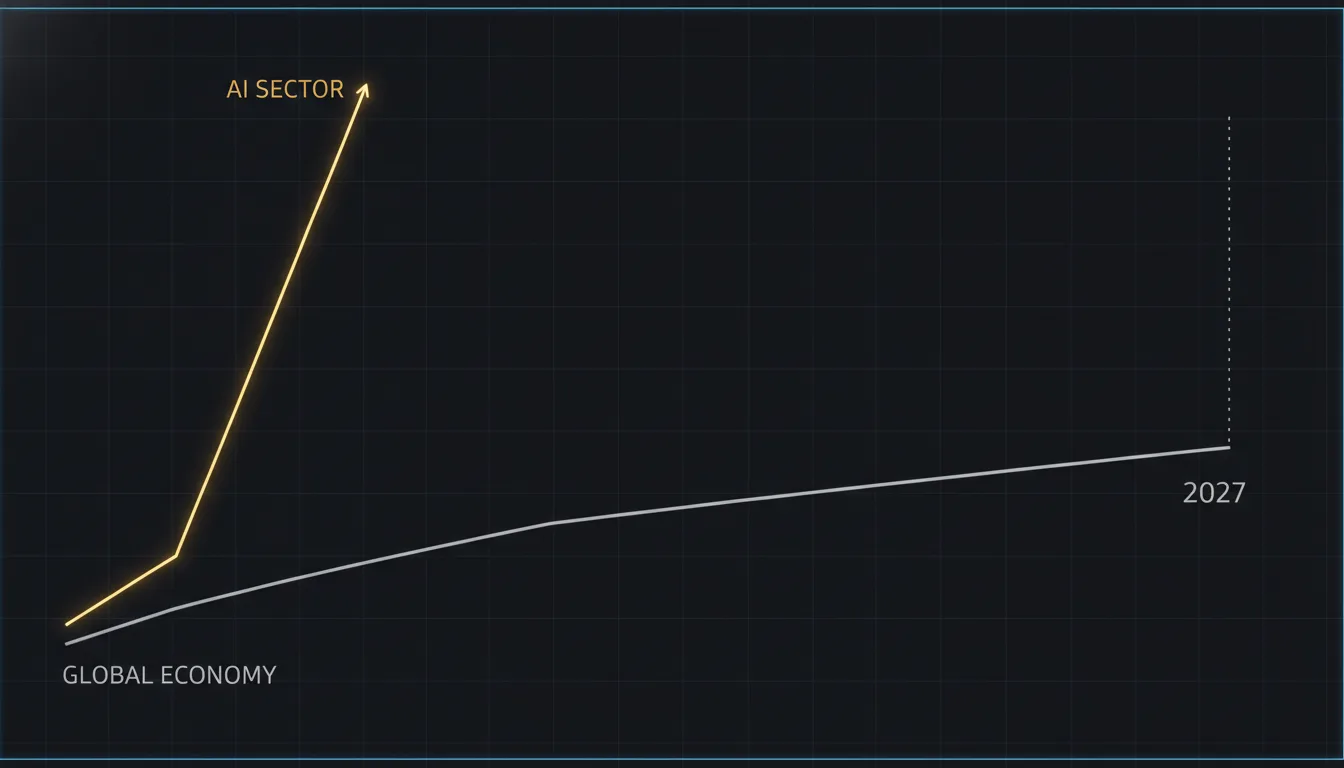

Goldman Sachs, in the same period, maintained its position that AI would not significantly lift the broader economy until 2027. Their "Tracking Trillions" report was characterised in many quarters as sceptical, even bearish. It was neither of those things read carefully. It was a timeline.

Both of these positions are compatible. The AI sector itself is growing at extraordinary velocity. Every other sector of the economy (manufacturing, services, healthcare, retail) is barely moving. The question is not whether AI is creating economic value. Clearly it is. The question Goldman was actually answering is when that value propagates outward from the infrastructure layer into the industries that will use it. Their answer was 2027. That answer is now one year away.

What Goldman Got Right

Reading Goldman's research charitably, as one should when assessing any serious institutional analysis, several of their positions hold up well against the evidence that has accumulated since.

The deployment timeline was broadly accurate. Mass enterprise AI integration has moved more slowly than the hype cycle of 2023–2024 suggested it would. The technology moved faster than the organisations. The MIT study of 300 companies in late 2025 found that only 5% showed significant profit impact from AI implementation, a finding that validates Goldman's caution about treating capability as equivalent to deployed economic value.

Their structural analysis was also correct. The current AI economy is, in significant part, a wealth transfer between and among large technology companies (hyperscalers, model providers, chip manufacturers) rather than broad-based economic growth. The Furman data confirms this: if a 4% sector is generating 92% of growth, that growth is highly concentrated, not diffuse.

Goldman's caution about bubble dynamics has been at least partially validated. Multiple AI infrastructure projects required hyperscaler backstops when projected revenue didn't materialise on schedule. Several large data center commitments were paused or restructured. The capacity buildout assumed a demand curve that has been slower to arrive than the infrastructure side anticipated.

What Goldman Missed (or Underweighted)

Institutional research has systematic blind spots, and Goldman's AI analysis is no exception.

The velocity of individual-level adoption was consistently underestimated. Consumer AI use grew faster than any enterprise forecast model predicted. ChatGPT was processing 2.5 billion queries per day by July 2025, a consumption level equivalent to the power output of a nuclear reactor, daily. That is not a niche tool. The productivity gains at the individual level are real even when they don't yet aggregate to GDP signal; GDP accounting was not designed to capture the value of a consultant finishing a report in three hours instead of eight.

The DeepSeek inflection was a genuine surprise to most institutional analysts. Goldman's capex projections were built on assumptions about frontier model training costs that reflected the OpenAI-scale infrastructure model. DeepSeek demonstrated in early 2025 that capable models can be trained and deployed at a fraction of that cost, which changes the economics of the entire sector in ways that hadn't been modelled. The competitive dynamics below the frontier shifted faster than expected.

And it is worth repeating: Goldman didn't say AI would never matter. They specified a timeline. The 2027 caveat was always the operative clause, and 2027 is now the immediate future.

The 92% Number Most People Ignored

"The data processing sector is only 4% of American GDP, but it accounted for 92% of GDP growth in the first half of 2025."

Harvard Economics Professor Jason FurmanThis is the most important data point in the 2025 AI story that almost nobody discussed in proportion to its significance. While commentators debated whether AI was overhyped, whether the returns would ever materialise, whether the enterprise rollout had stalled, the data processing sector quietly generated nearly all of the economic growth the United States produced.

That is not a bubble dynamic. Bubbles involve assets whose prices exceed the productive value they will generate. What Furman's data describes is something different: a sector that is generating disproportionate real economic output, while the industries that will eventually use what it produces are still in the integration phase. The sectors that build infrastructure grow before the sectors that use it. Railways preceded industrial growth by decades. The internet infrastructure build-out preceded the application layer boom by a similar margin. The ratio of 4% to 92% is not evidence of distortion. It is evidence of timing.

What the 2027 Window Means for You

We are, by most credible estimates, at the end of the infrastructure phase and the beginning of the application phase. The picks and shovels have been built. The models exist. The APIs are open. The question that 2027 will answer is which companies, industries, and individuals learned to use these tools effectively during the transition period, and which ones waited.

Goldman's 2027 estimate was not a warning about delay. It was a description of a timeline. Timelines are useful precisely because they give you a horizon to prepare for. The practical implication is not abstract:

- Learning AI tools relevant to your domain before the 2027 demand spike makes learning them competitive is an investment that compounds. The people who developed digital skills in 1995 were not competing against millions of equally skilled candidates in 2000. The same dynamic is playing out here, compressed into a shorter window.

- The infrastructure phase concentrated wealth in a small number of technology companies. The application phase has historically distributed value more broadly, to the businesses and workers who figured out how to use new infrastructure effectively. That pattern has precedent across every major technological transition.

- Goldman's blunt warning that displaced workers face long searches and worse conditions describes the average outcome, not the only outcome. The distribution is wide. The variable that matters most is whether you arrive at the 2027 application wave with relevant skills or without them.

The 92% figure is the part of this story worth returning to. The AI economy is already here. It's just unevenly distributed, concentrated in the layer that builds rather than the layer that uses. That distribution is a temporary condition, not a permanent one. The transition is finishing. The useful question is what you are doing in the remaining runway before it does.